Learning about finance in a new country can be very difficult for newcomers. As a Nigerian living in Canada, I grew up not knowing anything about credit card, mortgage, leasing amongst all the other terms that exist in the Canadian glossary of financial terms. I grew up knowing you only buy items if you have the cash for. Welp! Then I came to Canada, a credit society where I had to relearn everything I thought I knew about finance. I have brought Dr. Yewande Fadojutimi, who is a financial advocate and also a medical doctor. She previously shared a post on how to be a medical doctor in Canada. In this post, she breaks down how to navigate the financial system in Canada, which contains great financial tips for newcomers to Canada. Read the full interview below.

Introduce yourself

Growing up my family called me Yeye. They still do to this day. It’s short for my first name – Yewande. I’m Dr. Yewande Fadojutimi aka Dr. Yeye, your finance friend! You can find me on Instagram @dr.yewande or on my blog yeyefadoju.org. I’m a Medical Doctor and a Financial Literacy Advocate. What that means is, I help women navigate the world of personal finance here in Canada. I provide them with information so they can manage their money confidently, live debt-free and build wealth for themselves and their children.

As a medical doctor, a lot of people would be surprised as to why you are passionate about finance. What made you become passionate about finance?

You’re right. Medical Doctors earn a great income but are notorious for being terrible with their finances! It’s quite sad that after decades of hard work, many of my colleagues are forced to work indefinitely because they failed to plan appropriately for retirement.

For me, the journey started because I was always unsettled after leaving my financial advisor’s office. I barely understood what he was saying, and had no idea if my money was being invested appropriately. I had a nagging feeling I could be doing better with my finances, especially when I learned of a couple who retired at the age of 40 while working average government jobs!

So I decided to start educating myself, and realized that this was information EVERYONE needed to know!

Interestingly, I’m the daughter of a medical doctor AND a (retired) bank managing director. So perhaps it was only natural for me to represent both the worlds eventually.

Understanding the basics of finance as an immigrant can be challenging. What are useful resources that can help one get acquainted to finance in Canada?

I share tips on my Instagram page @dr.yewande and on my blog yeyefadoju.org. On my blog, there’s an invitation to sign up to join my inner circle. I send them emails every week that both teach and inspire them on their personal finance journey.

Another great blog to follow is: savvynewcanadians.com

There is a steep learning curve when it comes to personal finance and it can be quite intimidating. But the more you read the more it will make sense. The effort is really worth it.

How does one become financially responsible in Canada?

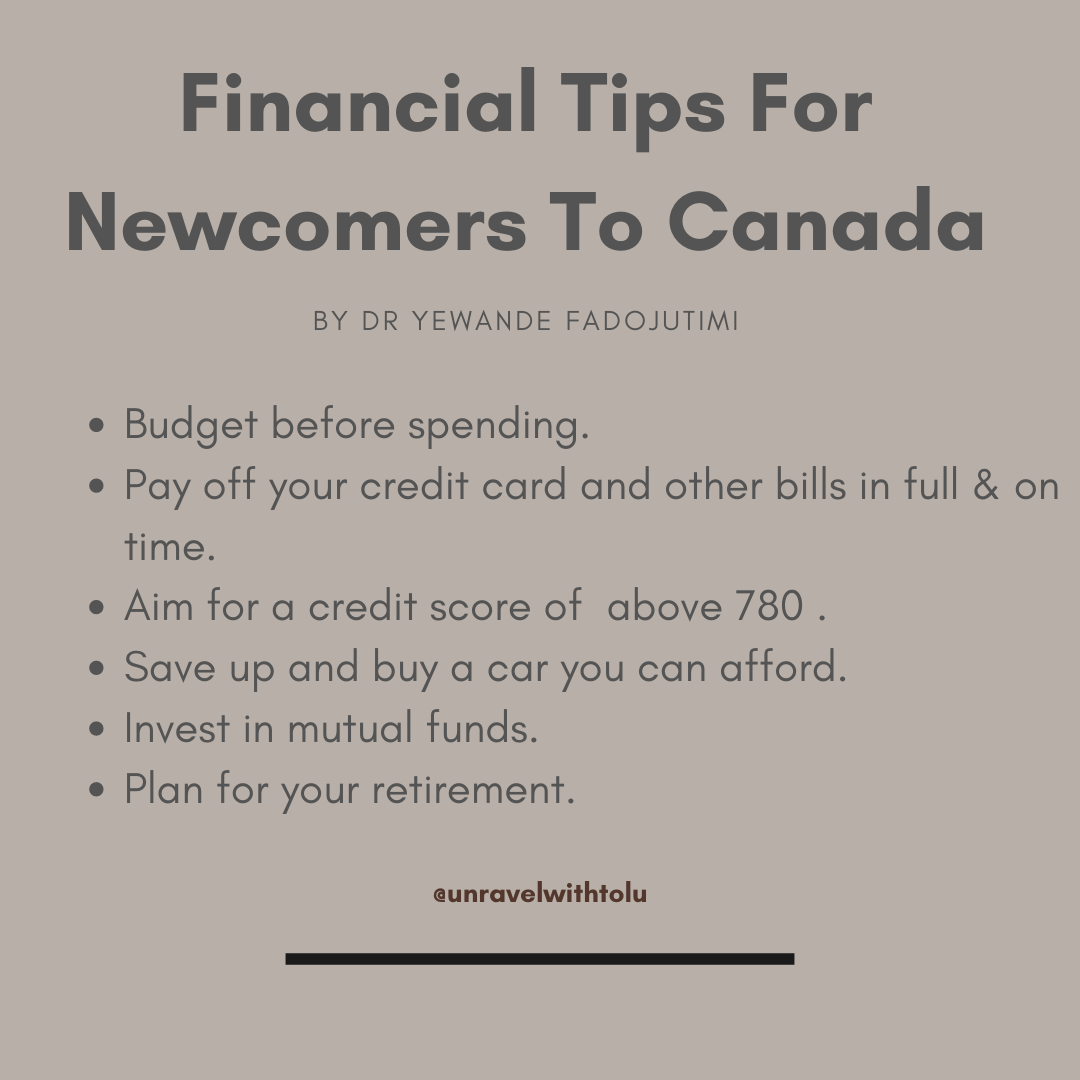

Do not use credit to buy anything that you do not have the cash to pay for. This includes any “buy now and pay later” schemes!

BUDGET ahead of spending. A budget is simply a money plan that tells your money where to go and what to do when it gets there.

Always allocate a certain amount of your income towards short term savings and long term investments (at least 10% each).

New immigrants come to Canada having to start over to build their credit score. What are the practical ways to build your credit score in Canada? What is the ideal credit score so newcomers do not get reckless in the process? What are the ideal practical tips for credit card utilization?

Credit is a very powerful tool that can be used for positive things. It can also be quite dangerous such that some people advocate that you avoid credit altogether. However, I don’t necessarily subscribe to that.

Your ability to handle credit demonstrates to lenders such as banks, that you are a responsible borrower. So when you eventually need a loan for school or a home purchase, a good credit score shows the lender that they are not taking a risk with you. They charge risky borrowers much higher interest rates than safe borrowers or deny them loans altogether.

The use of credit cards is one form of credit that will impact your score. Other forms of credit include utility bills and loans (e.g. a mortgage, student or car loans). The way you use all of these types of credit in combination will affect your score.

The easiest way for a new Canadian to build up their credit is to register for a phone plan and a utility bill under their name. Pay these bills in full and on time!

The next thing you can do is register for a credit card with NO ANNUAL FEES associated with it. If they have perks like cashback, free groceries etc, then that’s even better. But again, make sure the card comes with zero annual fees.

The most important piece of advice I will give anyone regarding credit card use is ALWAYS PAY IT OFF IN FULL.

Aim for a credit score above 780. It’s very important to check your credit score AND your credit report at least once a year.

How does one plan for their child’s education especially when one wants to give their children debt-free education?

My opinion might be unpopular but in this part of the world, I recommend that you establish a plan for your retirement before worrying about a debt-free education for your children. This is the reason why:

Although it’s not ideal, your children can recover from an education that was funded with some debt as long as you teach them solid financial principles.

However, imagine retiring at 60 and depending on your children for your cruises and beach vacations, your transportation, your manicures and pedicures, your dancing classes, to fund the business you’ve always dreamed of… All I’m saying is, if you’re forced to choose between debt-free education and retirement, please choose retirement first.

Wear your oxygen mask before attempting to put one on for your child.

You are big on investing rather than saving, why?

To clarify, I am big on investing for retirement, not saving for retirement. There’s a big difference. Saving for retirement won’t get you anywhere. I explain all the details here.

What can students and work professionals invest in?

To start, I recommend investing in a LOW FEE mutual fund (less than 0.5%), index fund or exchange traded fund (less than 0.3%). Stocks are fun to buy, but it is very, very hard to pick winning stocks on a consistent basis. If you are going to buy stocks, personally, I love dividend paying stocks and the Canadian banks (RBC, CIBC, BMO, Bank of Nova Scotia etc) have paid nice dividends over the years, even when the price of the stocks go down. Doesn’t mean this will go on forever though. (By the way, never take anyone’s stock recommendation at face value. Always do your research when it comes to buying stocks.)

Tax-Free Savings Account (TSFA) vs Registered Retirement Savings Plan (RRSP), which do you prefer and why?

It depends. If you’re a student in a lower tax bracket then a TFSA for sure. If you’re in a higher tax bracket and you’re looking for ways to minimize your taxes then fund your RRSP. Whatever you contribute to your RRSP will be knocked off your income for that year, meaning you will pay less taxes. That RRSP money is locked in until you retire though. There are 2 instances where you can use your RRSP money before retirement without penalty:

- The Life-Long Learning Plan and

- The (first time) Home Buyer’s Savings Plan

Buying vs Financing vs Leasing a car, which do you prefer and why?

Buy with cash if you are starting off in your personal finance journey. Save up to buy a car you can afford.

Financing is the next best option but finance a gently used car at a low-interest rate. And work to pay it off ASAP.

A car is not an investment so why pay interest on it?

Remember that once you drive the car off the lot its value plummets. Also realize that you still need to pay for insurance, maintenance and repairs. The more expensive your car the more expensive it will be to maintain. I’ve been driving the same Toyota Corolla for 10 years and I love it! It’s so reliable and Toyotas are now the model of choice for America’s millionaires.

Will I ever buy a luxury car? Maybe. But after my retirement is fully funded, my children’s legacy is taken care of, and I have experienced all the world travel I want to. God willing! This is how I’ve chosen to organize my priorities.

When it comes to purchasing a home, what is the most important thing newcomers to Canada should know?

Buying a home is not an automatic investment. The price tag on the house is not the final amount.

There are additional costs associated with closing the sale (e.g. lawyer’s fees). The bank will offer you a mortgage amount, please do not buy a house for this full amount!

Be open to living in areas that are not so “popular” right now.

When we moved to Canada 20 years ago, Markham (Greater Toronto Area) had a lot of open space and farmland. House prices have doubled in Markham since then. Milton (Greater Toronto Area) 5 years ago isn’t what it is now. House prices there have increased dramatically.

Don’t buy a house if you’re not ready to stay there for at least 5 years.

In Canada, we pay taxes on almost everything – food, bank account, groceries, income – the list is endless. How do you suggest one can pay less taxes on everything?

Taxes are unavoidable, however, the government gives us ways to minimize or refund these taxes via tax credits and tax deductions. This will depend on things like your income, whether you have children in the household, whether you have dependents with disabilities etc.

File your taxes every year, and file them ON TIME. Start the process on February 1st of each year, so you will have time to gather all the receipts necessary for any tax credits and tax deductions you are eligible for.

What are the practical steps one can take to successfully plan towards retirement?

Open a TFSA and allocate 10% of your income towards your retirement. Invest that money in a low-cost mutual fund, index fund or exchange traded fund every month.

Do not give in to panic when the market crashes. This is a natural phenomenon and crashes always recover. Stay calm and keep investing.

What is the one thing every resident in Canada should know about finance?

The way you think about money determines how you handle it. This is what I call “mindset”. If you keep telling yourself you can’t budget, then this will be your reality.

However, if you tell yourself that you can, then this will be your reality.

When I lack confidence, whether with finances or as a doctor, I adjust my mindset using affirmations like “I am a savvy investor” or “I am an excellent physician”.

I have a 14 day affirmation plan that my clients love using and I’m sure you will too.

Recommend a book for someone starting out the financial literacy journey.

So many to choose from!

Millionaire Next Door by Thomas J. Stanley if you are a professional that earns a decent salary but you’re not into budgeting and watching your account. This will motivate you to start.

The Richest Man in Babylon by George Samuel Clason was the book that started the journey for me, so I recommend it to all beginners.

post a comment

You must be logged in to post a comment.